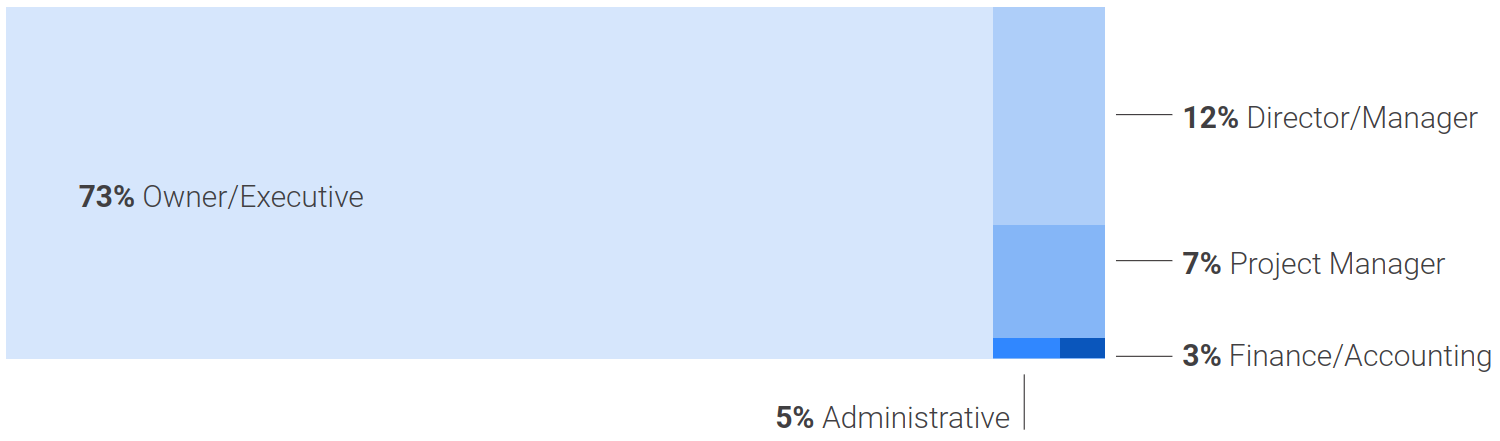

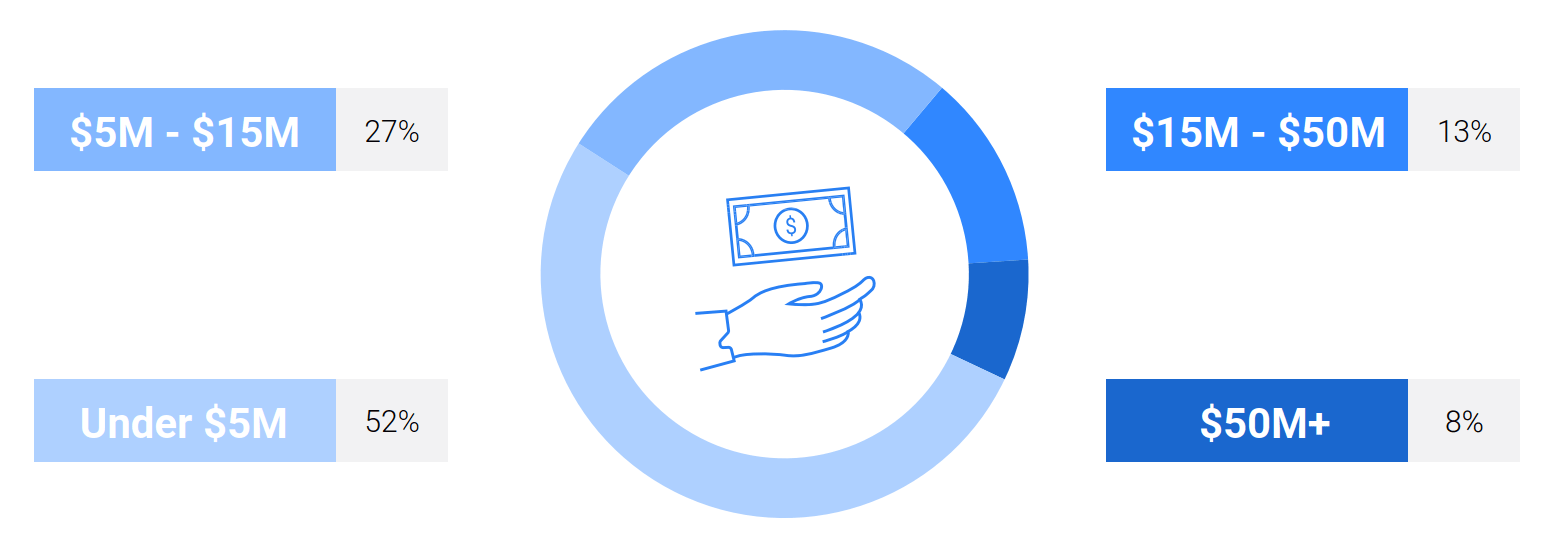

In January 2023, Billd conducted the third annual National Subcontractor Market Report survey. The resulting report investigates the economic realities of subcontractors across the country in 2022, zeroing in on the impacts of market conditions and industry trends on business growth, profit margins, and relationship dynamics. This year, nearly 900 subcontractors provided a wealth of perspectives and observations from their businesses, from which insights were summarized.

Subcontractors were the unspoken financiers of the $1.8 trillion construction industry in 20221, and bore the brunt of uncertain macroeconomic conditions. Their challenges reflect the most essential barriers and threats to prosperity in the construction industry. The single greatest obstacle for subcontractors this past year? Rising input costs outpaced bids.

1 April 3, 2023 release. https://www.census.gov/construction/c30/pdf/release.pdf

The overall decline in profitability is not unique to 2022. Not only is this the second consecutive year that subcontractors reported strained profit margins, but the figure also hasn’t changed a single percentage point.

The survey allowed us to dig deeper into the factors that created tight profitability, like the fact that subcontractors couldn’t adequately charge for rising expenses in their bids.

While the number of subcontractors concerned with material prices got cut in half this year, those concerned with labor shot up to nearly 50%. The trillion-dollar infrastructure bill, compounded with the regular flow of projects, means that hundreds of thousands of workers are needed to meet market demands. As older workers age and retire, the industry is spending more money to recruit, upskill, and adequately compensate new talent. The report highlights just how massive a concern this is for subcontractors.

The financial burden of material and labor has always been difficult to quantify, the full extent a bit hazy. Knowing that subcontractors spent an extra $97B almost feels like putting a face to a name. This $97B was subtracted directly from subcontractors’ bank accounts. For some, it’s the missing cushion in their profit margins. It represents 97 billion instances of subcontractors financing the entire industry, all while navigating uncertainty in their payment cycles and subpar access to capital.

We can’t talk about 2022 without talking about inflation. Inflation does play a role in the 97 billion additional dollars that subcontractors spent on materials and labor last year, but not as much as you’d think. This stat is all the more important because it outpaced inflation at a staggering rate. In fact, the year over year rate increase in material and labor spending is 2.5x greater than that of year over year inflation. This means that although inflation played a role, it’s not solely to blame. Material and labor costs within the construction industry simply rise far faster on their own.

To be clear, $97B isn’t what subcontractors spent on labor and materials in 2022. That’s just the extra amount they spent, on top of what they expected to (an increase of about 20.8%). Massive increases in the cost of labor and materials are to thank for that. So how did we arrive at this $97B figure? Let’s unpack it.

In 2022, the value of nonresidential construction was $888.5B.2 With a conservative 80% pass through of costs from GC to subcontractors, we estimated commercial subcontractor revenue to be $710.8B. Assuming a 66% expense distribution towards labor and materials, without price increases, $469.1B would have been spent ($234.6B on materials and $234.6B on labor).

However, according to our survey, labor spending increased by 15% and material spending increased by 26%. Therefore, subcontractors spent $270.4B on labor and $296.1B on materials. Ultimately, they spent $566.5B, shelling out $97.4B more than they expected to.

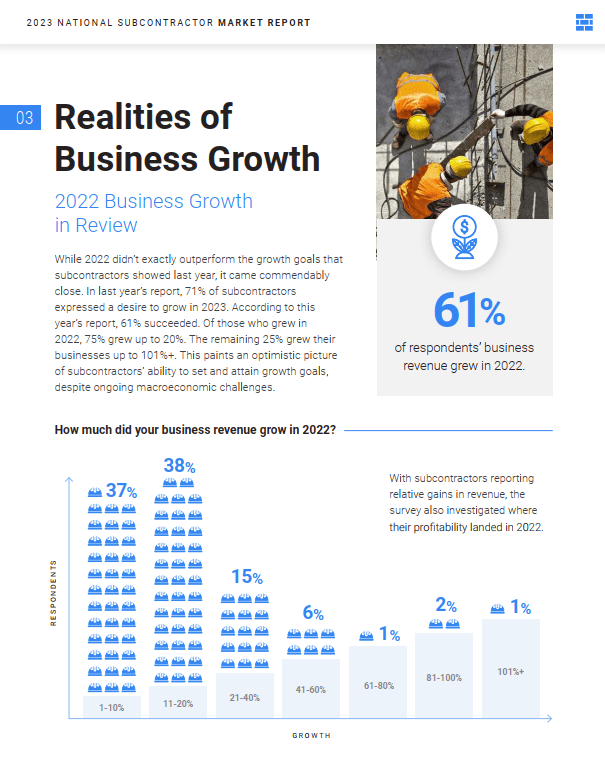

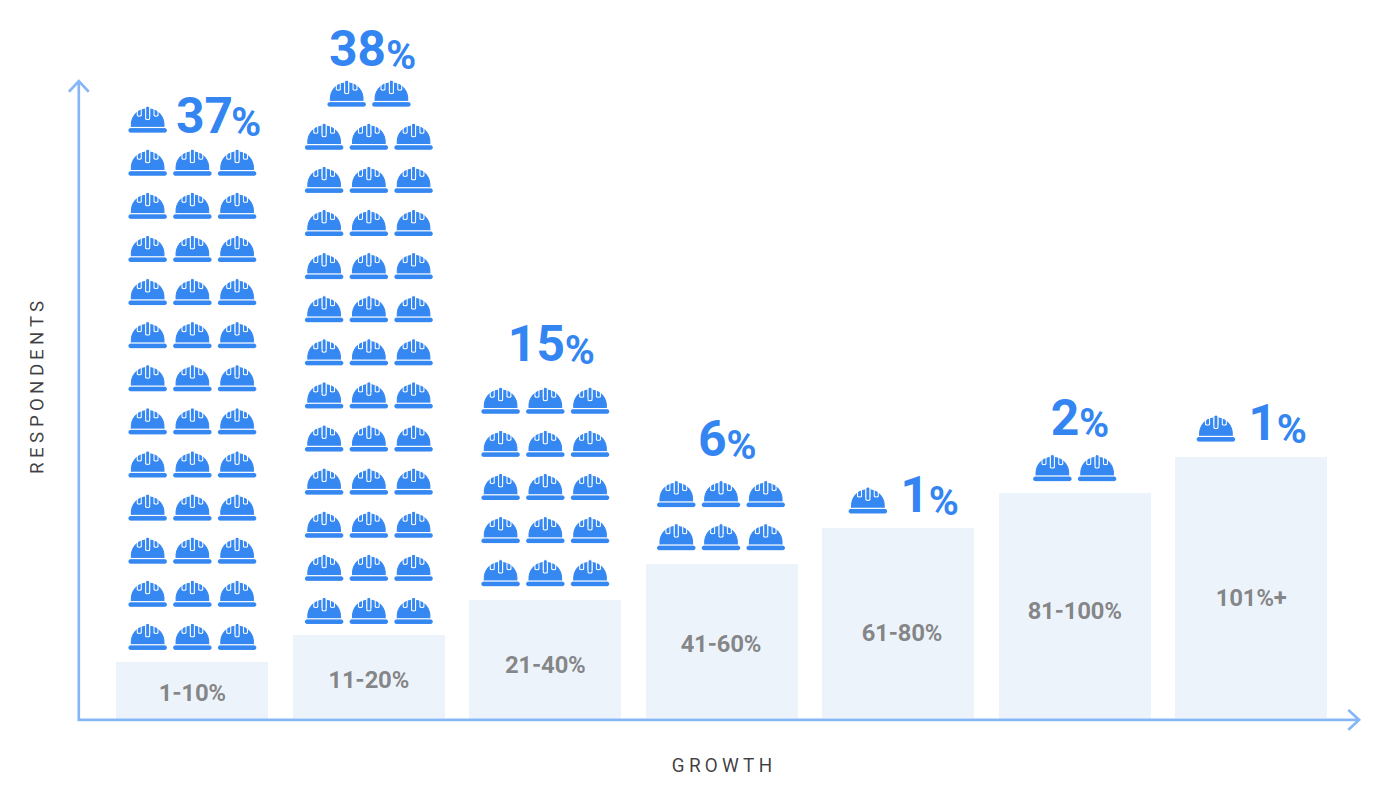

Despite the industry challenges they face, subcontractors are still determined to make the best of 2023. Respondents showed interest in growing their businesses, in line with how they’ve responded year after year. More subcontractors appear interested in going after larger projects, provided they have sufficient profit margins.

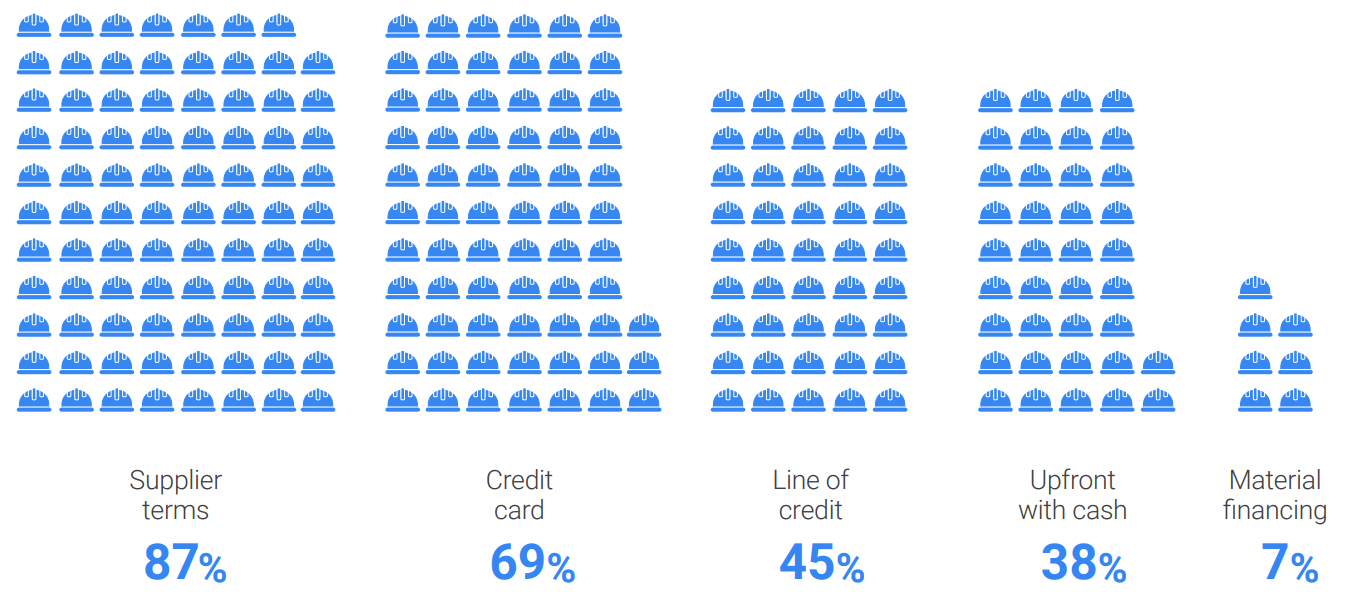

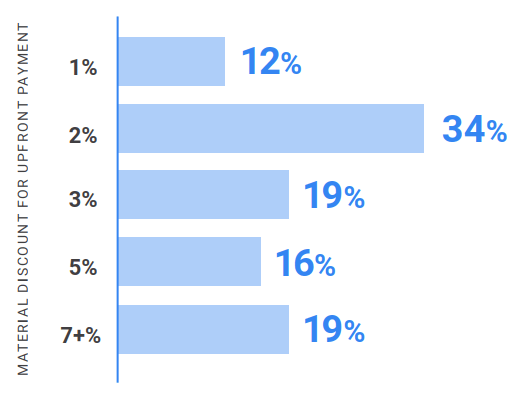

Arguably the most cash-flow-friendly financing option for subcontractors, material financing remains the least leveraged, yet more than double the respondents from the survey claimed they’ll be leveraging it in 2023, compared to 2022. It’s the largest untapped opportunity for subcontractors to extend their term length while leveraging the same supplier discounts they would get for paying upfront in cash.

Subcontractors have been forced to finance the construction industry, despite them doing the actual work. Their ability to pull through is crucial to industry survival. To beat narrow profit margins, high material costs, and slim labor availability, subcontractors need good financial resources. But many of the options available aren’t tailored to the construction industry. New financing options can help subcontractors navigate industry-specific challenges. It’s important to make subcontractors aware of these financial options at their disposal, rather than letting them default to a growth-hesitant mindset. Those tools are Material Financing and Pay App Advance by Billd.

We’ve told you how Material Financing can facilitate smooth procurement and maximize discounts. Pay App Advance helps subcontractors get their pay app funded the day it’s approved, rather than waiting months at a time. Subcontractors then have a comfortable window to pay Billd back, which gives them more time to receive payment from the GC. This affords subcontractors greater financial predictability around their receivables, and allows them to cover their largest, immediate expenses with greater ease.

In recent years, construction has adopted new technology and software to streamline business operations. More than half of all subcontractors surveyed use estimating and accounting software, making it the most prevalent form of construction technology to date. If subcontractors are willing to adopt new practices that help them proactively manage their business outside of financing, it’s only logical to make similar advancements in their financial operations.

Without subcontractors, construction can’t happen – and in more ways than one. In addition to the materials, labor and expertise they deliver, the capital provided by their businesses is critical to supporting projects from groundbreak through completion. Yet every year we see macroeconomic conditions compounded by long standing industry practices that make the subcontractor-as-a-bank model harder to maintain for the sub.

Their uphill battle is as steep as ever. This year we saw subs’ supplier terms be cut, making those terms even more inadequate against even longer AR timelines. Their direct costs have increased to the tune of $97B, but their bids and contracts can’t always keep up. What’s worse is that most GCs will not provide the contract provisions to the sub to ensure they can pass price increases to the property owner.

That means the cushion of cash in the business – their profit – is being squeezed to its limit. If that wasn’t enough, in 2023 we continue staring down the barrel of significant labor shortages and premiums. Something’s got to give… and it will.

We at Billd can’t fix inflation, material volatility, or a thinning labor market. But, we can get subs access to working capital that will make these challenges less consequential. And, we can make sure subs know the cost of all financing (Billd products, cost of cash, cost of supplier terms, cost of bank line of credit, etc.) and include that cost in their contracts. Tools that provide the flexibility to pay upfront with terms that align with their payment cycles can help subs survive a volatile material market. The cost of financing can easily be offset by adding it into their bids. This type of cash flow flexibility will actually give way to profitability – and that’s what subs need.

When it comes to obtaining working capital, subs aren’t in an ideal position. They generally carry low cash balances, are owner operated, have unpredictable AR, and are not well understood by the traditional institutions that could fill their working capital gaps. These factors contribute to the fact that nearly a quarter of subs find it difficult to obtain new sources of financing. This can hurt their ability to achieve their profitability and business growth goals at large. We never want subcontractors to limit their growth because of something as conquerable as access to capital.

Subcontractors built America, and here at Billd, we don’t think they should be deprioritized for financing, project payment timelines, or material purchasing power. And because we believe that, we back it up. I’m proud to operate a company that exists to champion the subcontractor. Billd will be here to serve as your partner in profitability, progress, and prompt payment.

Christopher Doyle is an entrepreneur and business leader with extensive construction and finance industry experience. He is the co-founder and CEO of Billd, a disruptive payment solution for the construction industry that helps subcontractors grow their businesses with less hassle and risk. Recognizing the cash flow hurdles that contractors face, Doyle launched Billd to make traditional Wall Street working capital accessible to business owners in the construction industry.

Billd stands alone as a partner that truly champions the subcontractor. Their financial and payment products empower subcontractors to bypass project hurdles by providing access to upfront funds to cover their most pressing costs, including materials and labor. Unlike traditional financing outlets, Billd provides flexible lines of credit to accommodate the unpredictability of cash flow in construction, and extends their customers up to 120-day terms to align with industry payment standards. Billd knows traditional credit metrics are poor predictors for risk and has built a variety of industry-specific, proprietary analytic and financing tools to allow subcontractors to stabilize cash flow and more effectively grow their businesses.