Every construction subcontractor faces the same fundamental dilemma: needing to pay for materials, labor, and general and administrative expenses each month, while not getting paid for completed project work for 60-90 days. No matter how new or established your business may be, cash-flow issues do not discriminate in the construction industry.

As a growing construction business, you’ll eventually need to establish large credit limits to run your business. But how do you get there?

While there are several financing options to bridge the cash-flow gap, whether or not each one is a smart move (or even an option) for your business all depends on your current stage of business growth. More established subcontractors have a variety of options at their disposal, but when you’re just starting out, it’s tough to get the financing you need to succeed. When you’re an up-and-coming construction entrepreneur, the question is: how do you access the construction financing options available to the major players and utilize them to scale your business?

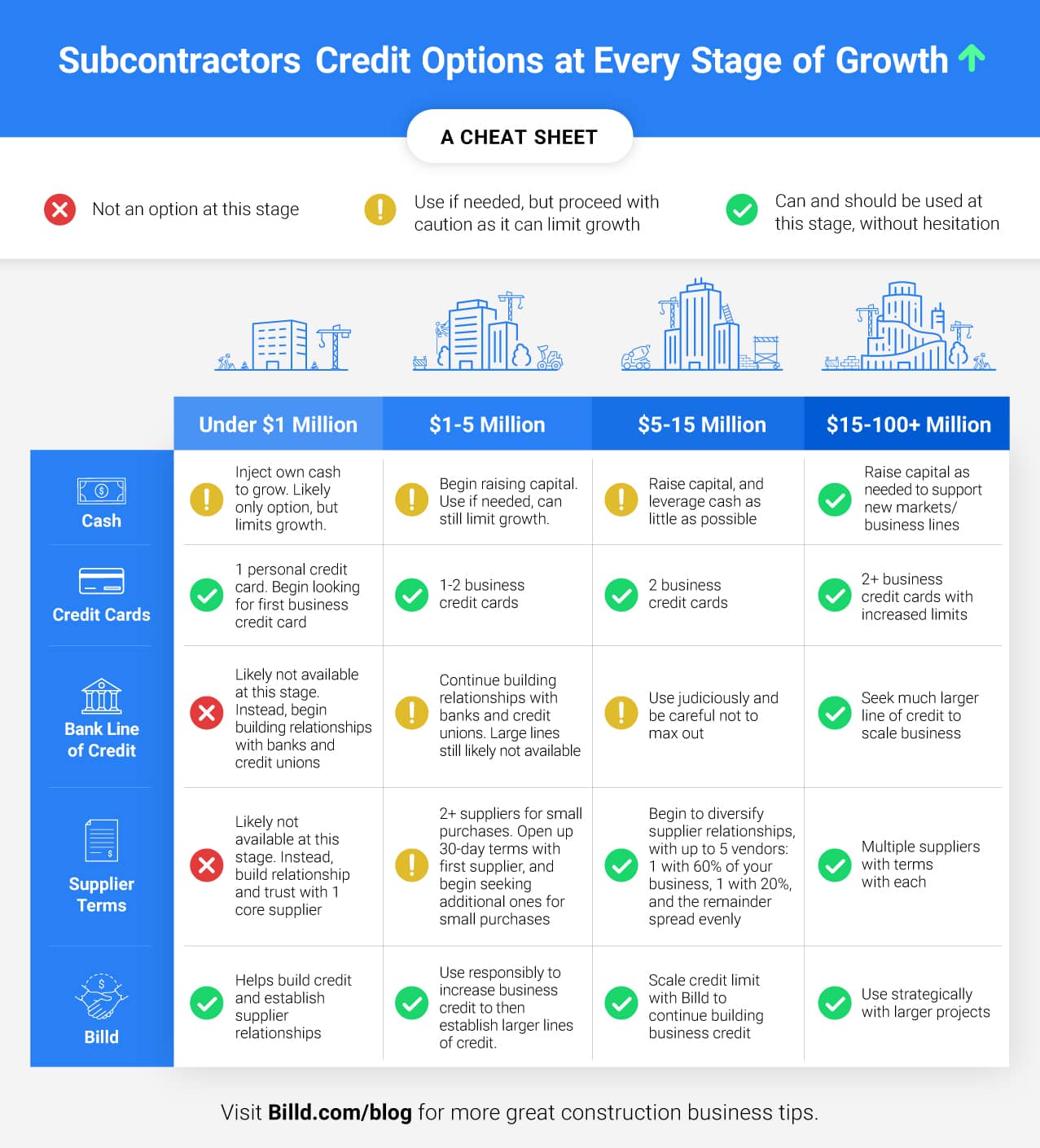

Let’s take a look at five common types of construction financing—cash, credit cards, banks, supplier terms and contractor material financing with Billd—and how to most effectively approach each option at four stages of growth.

Table of Contents

Under $1 Million Contractors

The most successful construction entrepreneurs aren’t just good at business development and sales—they’re also smart about addressing cash-flow challenges early on. However, for new business owners, this is often no small feat.

Here are your financing options when you earn under $1 million in annual revenue.

Cash

✔️Option

When you’re financing your business with cash, you’re likely using your own personal cash, equity dollars that you’ve raised from investors, or cash that’s been generated from sales. While these are likely the only options early on, they’re suboptimal ways to grow your business at an early stage, primarily for two reasons:

- Taking on investors early on means giving away a large chunk of your business that could become very valuable down the line.

- When cash is being used to finance your business, you forgo the opportunity to use that cash to take on larger projects, more projects, or investing in marketing and sales initiatives.

Credit Cards

✔️Option

At this stage, you’re most likely relying on personal credit cards to purchase materials and pay for everyday expenses. But by the time you reach the $1 million mark, it’s critical to get a business credit card and use it. Pay for recurring expenses like utilities and contractor management software, and then pay it off each month. This will help you build a positive history with the (business) credit bureaus in order to secure additional credit and better terms down the road.

One important factor to consider are credit card fees. Some merchants will build in a 2-3% additional fee to the cost of their products or services for credit card payments, so understand that you are paying those fees when you use credit cards.

Bank Line of Credit

❌ Not an option

You’re simply not getting a bank line of credit at the sub-million stage, or it’s very unlikely. However, there are steps you can take today that will lay the groundwork for future access.

1. Choose the right bank

Find a community or regional bank with a reputation for providing strong line-of-credit options for business owners in the construction industry.

2. Develop a long-term relationship with your banker

Introduce yourself and give your banker a full picture of where your business is now and where you hope to be. Share information about your projects you’ve done, what you’re bidding on, customers you work with, your business projections, and financials. Transparency is key!

Do not ask for a bank line of credit yet. This is just about setting the stage so that, later on when you do apply for a bank line of credit, you will have a history of working together.

3. Start a conversation about a future bank line of credit

Let your banker know you’re working towards a line of credit one day, though you realize your business doesn’t command it yet. Ask them what it would take to secure a bank line of credit in two years…and, guess what? They will tell you. Then you’ll know exactly what you need to do to build their trust and gain access.

Remember: as much as credit and risk are driven by algorithms, people run them. Building a relationship with your banker early on will help position your business for success.

Supplier Terms

❌ Not an option

Supplier terms are normally not available at this stage—but by developing a solid relationship with a supplier, you can eventually secure terms when your business is ready.

How to Approach Suppliers You Haven’t Worked With

Introduce yourself to a new supplier just as you would with a banker: be transparent, let them get to know your business, and whatever you do, don’t ask for a credit line yet. First, build your purchase history with them. Start with small orders you can purchase with cash or credit cards. If you don’t have the cash flow or credit to accomplish this, working with Billd will enable you to pay cash upfront for materials while repaying us on more flexible terms.

Once you’ve established a relationship, start the conversation about securing terms. If you’re working with Billd, let the supplier know you’re leveraging another financing option to purchase materials, but that you would also like to get to the point of having 30-day terms with them as well. Don’t be afraid to simply ask what it would take to secure terms.

However, don’t rush into a supplier relationship—because you may not be ready for it. As the owner of a sub-million dollar construction business, one missed payout can catastrophically disrupt your cash flow. When a supplier does extend a line of credit to you at 30-day terms, they’ll be watching closely to see how you pay. If a cash flow problem causes you to miss a payment, it could ruin that relationship.

Billd

✔️Option

If your revenue is between $500k-$1 million and above, Billd is an option for you . At this early stage in particular, Billd doesn’t just make sense—it’s the best option. When you start a relationship with us early on, we’ll help you quickly build a purchase history with your supplier until you can achieve a more sustainable approach. Additionally, Billd reports to credit bureaus to help you establish your business’s credit history.

Here’s how it works: we pay your material supplier upfront in cash and you pay us back on flexible 120-day terms, or when you’re paid for your work (whichever comes first). You get your materials when you need them, and you never miss out on new or bigger projects due to cash flow bottlenecks, so your business can continue growing.

How Billd Improves Upon Supplier Terms

1. Reporting to the credit bureaus

We report to the credit bureaus, while suppliers usually do not. Why is this significant? You need a good credit history to get a company credit card and bank financing as your business grows. If you’re purchasing materials through supplier terms, that’s doing nothing to improve your business credit score. With Billd, we strengthen your financial position from day one.

Think of a relationship with Billd as planting a small seed for the success of your business—do it early and watch it continue to grow.

2. Cost savings

Most suppliers offer a 2-3 % discount on upfront cash payments. But in reality, this is an added charge for financing—sort of like those credit card fees. When you buy on terms with your supplier, you pay more.

If you’re purchasing $100k worth of materials per month on supplier terms, and that supplier offers a 2% discount on cash payments, it’s actually costing you an extra 24% annually. Here’s the math – $100k x 2% = $2,000 cost for buying on terms. 2% for 30 days means if you annualize that, it comes to 24% (2% x 12 months).

3. Greater flexibility

Why pay through suppliers on fixed 30-day terms, when Billd offers comparable rates at 120-day terms? Plus, we provide a much higher credit limit than suppliers are usually able to offer.

$1-5 Million Contractors

At this stage, your business needs to be setting itself up for the next phase of growth, and establishing relationships with suppliers, bankers, and partners to give you the credit limits needed to continue growing. Here’s how your financing options may change in the next phase of your business.

Cash

✔️Option

Cash is an option at any stage, but In the construction industry, relying on cash flow is dangerous as payments are inevitably unpredictable, and expenses tend to come due far before revenue is realized. Additionally, raising equity and using equity dollars can be very expensive as your business is primed to continue growing.

Credit Cards

✔️Option

You should be ramping up your business credit card, spending a significant amount and paying it off every month. While you could get a second card, splitting up your spend might make you less attractive to your primary credit card company, negatively impacting your strategy to build up to larger credit limits.

One thing to note: When you’re under $25 million, your debt is going to be collateralized by a personal guarantee, which means you’re putting your personal finances on the line. Get to know your business credit card account representative and make sure they know your story. When your business reaches that $25 million mark, inquire about options for removing the personal guarantee.

Banks

❌ May or may not be an option

While you’re likely still not eligible for a bank line of credit, check in with your banker every six months to continue building your history together. If you are able to secure a bank line of credit, it’s likely going to be fairly small and probably not enough to leverage the power of debt to start growing your business.

Supplier Terms

✔️Option

Now that you’ve developed a solid relationship with one supplier, it’s time to start diversifying. Approach additional suppliers the same way you approached the first — by starting an open dialogue about your business and future goals. Tell them the other supplier has been great, but you’re looking to expand your options. Start with small purchases and build up. Once you’ve secured terms, find out how they might change in a few years when your business has grown.

Billd

✔️Option

Don’t forget: if you’re not paying cash upfront for materials, you’re likely paying an extra 24% annually. Billd enables you to save money on materials, bridge the cash-flow gap from construction payment cycles, and strengthen your credit score, all while still building relationships with suppliers.

$5-15 Million Contractors

Cash

✔️Option

You might want to look at raising capital at this stage if you’re growing fast, but consider debt options as well.

Credit Cards

✔️Option

You should still have one or two credit cards and really know your account rep well by now. Your credit limits should be consistently growing as you continue to repay balances monthly.

Banks

✔️Option

This is when your relationship with your banker kicks into high gear and you can have a real conversation about getting a large bank line of credit. You’ll need sound financial statements and credit history, which you’ll have if you’ve been paying off those credit cards and purchasing materials through Billd. A personal guarantee is still required until you break that $15 million barrier.

Supplier Terms

✔️Option

You probably have at least five vendors now, including a primary with 60% of your business, another with 20% of your business (perhaps specialty items), and the rest you either spread out evenly or don’t use at all. Make them work for your business! Fill out credit applications, get on their radar and let the sales reps call on you. Start having conversations about pricing with your suppliers to ensure you’re paying a comparable rate to your competitors.

Billd

✔️Option

At this stage, it’s critical to keep diversifying your financing options. If a project payment doesn’t come through for 90 days but your supplier bill for $500k is due in 30 days, you’ll be stuck in a major bind. In addition, if you’re relying on supplier terms for materials, you’re still paying an extra 24% annually and the payment cycle still requires you to pay for materials before getting paid for the work.

Having only one financing option could leave you high and dry, but utilizing a mix of supplier terms and Billd will help mitigate those cash-flow problems. At the very least, get pre-qualified and on our platform so you have the option when you need it.

$15-100 Million+ Contractors

Not only do you have access to numerous financing options at this stage, but once you get to more than $100 million in annual revenue, you can also start pressing for the best pricing and terms.

However, there are also snags and pitfalls you’ll begin to experience at this stage. Someone could get injured on the job and sue you. The general contractor or property owner on a huge project could go bust and never pay you for your work. There are always unexpected occurrences in business—but now they’re on a much larger scale, so it’s more important than ever to have a variety of different financing options to survive.

Cash

✔️Option

Again, cash is always an option, but you’re either giving away portions of your business or leveraging cash flow from operations that are more efficiently used elsewhere.

Credit Cards

✔️Option

As a strategy to increase your credit rating, talk with your primary bank about increasing your credit line considerably—whether you need it or not. You’re likely extremely busy at this stage, so force yourself to do this if necessary. Much like working out to stay physically fit, you have to be consistent, over time, to build your company’s strength and financial fitness.

Banks

✔️Option

Getting a bank line of credit should be an absolute slam dunk by now. Don’t push too hard on a rate yet—but do make sure you use it to optimize your business. Pay suppliers upfront with your bank credit lines to get the most competitive prices, but don’t max it out so you can maintain a cushion for unexpected business turbulence.

Supplier Terms

✔️Option

Try pushing your primary supplier a bit to ensure you’re getting the absolute lowest price, or reducing the amount of materials you source from them down to 50 percent to diversify your options. Other suppliers are likely taking notice of you and trying to get your business. As they contact you, be transparent about what your business goals are and what you expect from them (reliable service, strong pricing and good terms), and stay consistent on this messaging.

Billd

✔️Option

Billd is a valuable option for larger subcontractors for several reasons, such as improving your credit, having diverse financing options to avoid cash-flow bottlenecks, and getting the lowest price on materials. When you’re making a $1+ million material purchase, having to come out of pocket for that in 30 days before you’re paid the $2.5 million in revenue could be a stretch and put you in a financial bind, even at this stage.

No Matter Your Stage of Growth, Reach Out to Billd Today

We have decades of experience in the construction industry and work with thousands of subcontractors at all stages of growth, so we know the challenges you face first-hand.

When you work with us, you’ll gain access to a higher credit limit than any other option out there, with flexible terms, so you can build relationships with suppliers, build your credit history, and get the lowest rates on materials you need to take on more, bigger projects. Whether you’re just starting out or bringing in more than $100 million in revenue annually, our payment solution will help strengthen your financial position significantly so you can focus on growing your business. Ready to grow with Billd?