As early pay programs mature, the conversation naturally shifts from why to how. Clear objectives and timing set the foundation, but long-term success depends on how the program is funded. The right funding strategy doesn’t just support operations; it determines scalability, risk exposure, and overall financial performance.

In this second installment of the series, we examine the funding strategies that power sustainable early pay programs. From longevity and scalability to liquidity risk and controls, we’ll explore how strategic funding design can strengthen margins, preserve flexibility, and position your program for durable growth.

Table of Contents

The Importance of Choosing the Right Funding Strategy

Creating clearly defined objectives will give GCs the right foundation and internal alignment regarding what the early pay program is meant to achieve. Once that is done, the next critical step is to decide how to fund the program.

Early pay programs are funded programs, regardless of the source. To generate margin, improve subcontractor stability, or reduce project risk, capital must be deployed to pay subcontractors earlier than the contractual maturity date. How an early pay program’s capital is sourced has long-term implications for scale, risk, and sustainability.

One thing is certain: A general contractor’s cash demands and priorities change from year to year. A funding strategy that works well in one period may be less practical in another. Building flexibility into program funding is an important consideration that is often overlooked or not fully analyzed.

For CFOs, this is a strategic decision, not a tactical one.

Using Internal Cash (Self-Funding)

Many general contractors initially fund early pay programs using their own cash. The logic is straightforward: Idle cash sitting in bank accounts often earns relatively modest returns. By comparison, early pay programs can significantly improve the yield on that cash, often doubling, tripling, or more what is earned through traditional cash management strategies.

Using internal cash can be effective, particularly in the early stages of a program or when objectives are limited. However, there are several important considerations.

Considerations when using internal cash include:

- Program longevity: Early pay programs often run for many years. A successful program today may still be operating 10 or more years from now. GCs should consider whether excess cash will consistently be available over that timeframe.

- Competing uses of cash: Cash has both ongoing and evolving demands.

- Ongoing cash needs include salaries, benefits, taxes, 401k contributions, bonuses, and operating expenses.

- Evolving cash needs include growth initiatives, technology investments, operational improvements, acquisitions, and risk mitigation.

Committing cash to an early pay program may reduce flexibility in other strategic areas.

- Concentration and liquidity risk: Using internal cash increases concentration risk. Depleting cash reserves to fund subcontractor payments can reduce financial buffers during downturns, project delays, or unexpected events.

- Scalability constraints: If the early pay program’s objective is a significant margin, which requires broad adoption, internal cash may eventually become a limiting factor. Using $10M in cash to fund an early pay program may be manageable. However, strong adoption can quickly increase liquidity needs to $50M or more—depending on the GC’s size—which may not be manageable.

This raises a strategic question: Is the organization willing and able to commit that level of capital on an ongoing basis? Self-funding early pay programs is often the result of success. However, success without funding durability can create new constraints.

How to mitigate cash exposure

Some organizations limit program size or allocate a fixed amount—for example $10M—to test utilization. While this approach controls financial exposure, it may also limit adoption and hinder the achievement of stated objectives.

If exposure is deliberately limited, program goals should be recalibrated accordingly.

Working With a Financial Partner (Third-Party Funding)

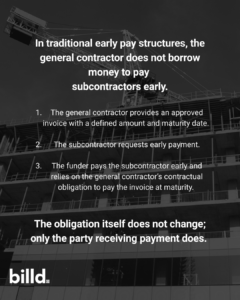

An alternative approach is to use third-party funding. Under this model, a financial partner pays subcontractors early using its own capital.

The general contractor provides approved invoices and continues to pay them upon maturity. In return for facilitating early payment, the general contractor receives an economic benefit (a rebate) without having to deploy its own cash. A consideration for the GC is that the rebate received will be less than what is earned if they use their own cash, as the funder must be paid. However, the GC is earning significant revenue from issuing approved invoices, and the program has no cash implications.

Who are these third-party funders?

These financial partners are typically banks and funding institutions that are comfortable underwriting the general contractor’s credit risk. In many cases, they include the GC’s existing bank relationships. In other cases, they may be other banks or non-bank funding institutions that specialize in or prefer supply chain finance-style programs. What matters most is that the funder is underwriting the general contractor’s ability to pay approved invoices at maturity, not the subcontractor’s credit profile.

It’s important to note that third-party funding does not mean the GC is giving up program control. In third-party funded programs, the general contractor controls:

- Which subcontractors are eligible to participate

- Which projects are included in the program

- Which invoices are eligible for early payment

- How much total exposure the program allows

Third-party funding changes how the program is financed, not how it is governed. This flexibility allows general contractors to scale or contract the program over time without tying participation to internal cash availability.

Is it considered borrowing?

A common concern is whether third-party funding represents borrowing. When structured correctly, it does not.

This structure is consistent with over 20 years of established supply chain finance practices across multiple industries and is fundamentally different from borrowing.

Choosing the Right Approach

There isn’t a single correct approach to funding. Organizations typically choose one of three strategies:

- Internal Cash: Relying solely on the company’s own funds.

- Third-Party Funding: Depending entirely on external sources.

- Hybrid Approach: Using internal cash to a point they are comfortable, and supplementing with third-party funding to manage growth and scale.

The key criterion for success is alignment. The funding strategy should support the objectives established for the early pay program, provide flexibility as business conditions evolve, and ensure the program’s long-term sustainability. When evaluating early pay solutions, ensure the provider offers multiple funding options to meet your evolving cash needs because early funding decisions have a lasting impact by shaping adoption rates, risk exposure, and overall outcomes for years to come.

With objectives and funding strategies decided, GCs are ready to look at the next key to success: subcontractor adoption. In the next article in this series, discover why high adoption rates among subcontractors can make or break your early pay program, and how a facilitator can bridge the gaps.