Billd surveyed subcontractors nationwide in 2024, analyzing their responses to build the 2025 National Subcontractor Market Report.

Each year, the survey digs into the financial and economic conditions of commercial construction subcontractors.

Over 800 construction professionals, 88% of which have been in business for 10+ years, lent their perspectives to create this year’s report.

The stats from this year’s report reveal a familiar picture: Slow pay and cash flow strain are keeping profits stuck in subcontracting businesses.

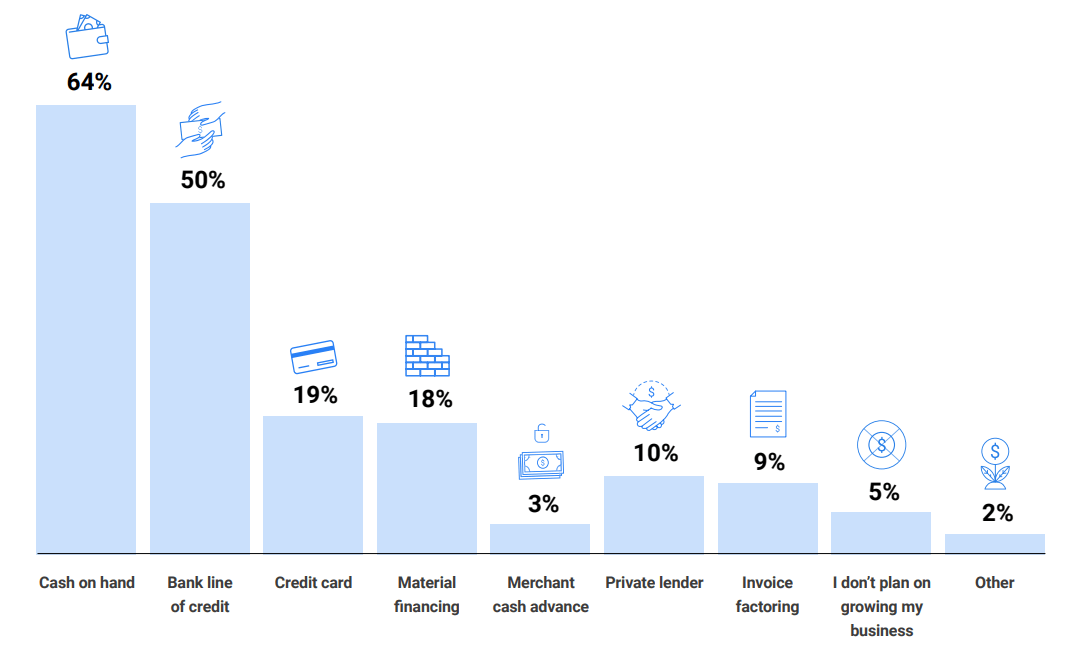

In 2024, Billd authored a guide on how to build a capital strategy that allows subcontractors to operate efficiently despite cash flow unpredictability. It starts with obtaining a variety of working capital options, including cash, supplier terms, bank lines of credit, credit cards, and construction-specific financing options. This last one is important because traditional financing options are not catered to construction, making them less than ideal because they have limits that don’t meet the needs of construction businesses. By maximizing credit availability across a diverse set of capital options, subcontractors can create a safety net that becomes the foundation for growth.

The combined impact of these options depends on how and when they are deployed. The rule is simple: Use the least flexible capital options first, and the most flexible options last. For example, supplier terms are rigid in that they can only be used for one type of expense, there are time constraints on when they can be used, and they can only be used for so long. Therefore, using those first instead of a more flexible option ensures you’re not fo

The survey results reveal the severity of the issue and how widespread it is. The stats also underscore that it’s an issue not well understood by general contractors.

That 26-day perception-versus-reality gap is not insignificant to the subcontractor businesses waiting for payment.

Subcontractors wait on average 56 days to get paid after they submit a pay application, consistent with the average of 57 days in the 2024 National Subcontractor Market Report. Even as technology advances to streamline the payment process and general contractors have become more aware of the impact slow pay has on subcontractors, the problem is still rampant. The end result is growing pressure caused by the funding gap.

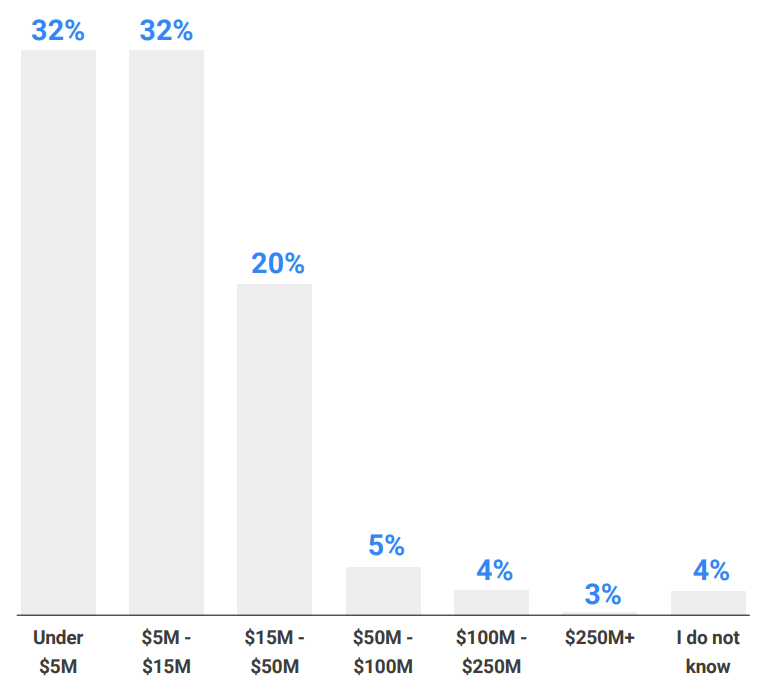

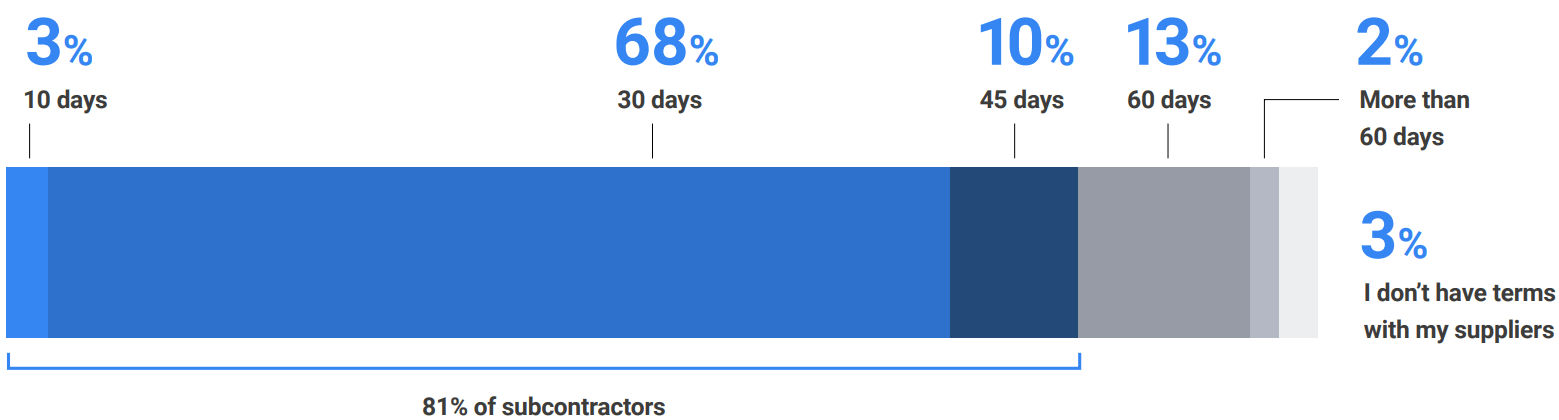

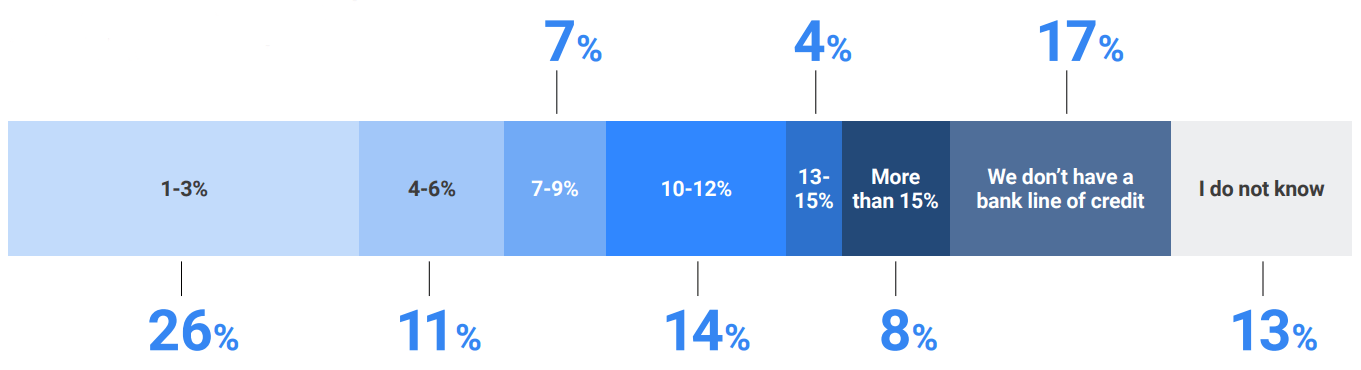

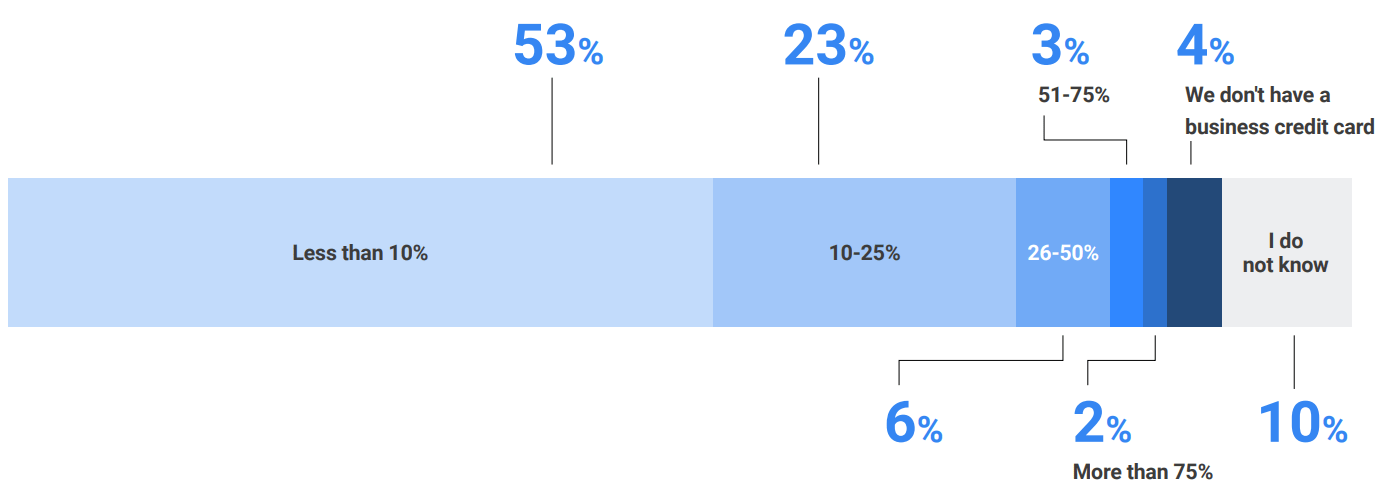

The funding gap represents the financial deficit between the amount of expenses subcontractors need to fund, and how much capital they actually have at their disposal between available working capital and cash from their projects. Funding gaps are a pervasive issue that affect subcontractors of any size, from $5M in revenue to $100M in revenue, because the issue is rooted in the faulty mechanics of the industry. For subcontractors, vital cash is often tied up in late payments from GCs and traditional working capital solutions are limited in what they can offer. The statistics below illustrate the shortfalls in funding that subcontractors deal with.

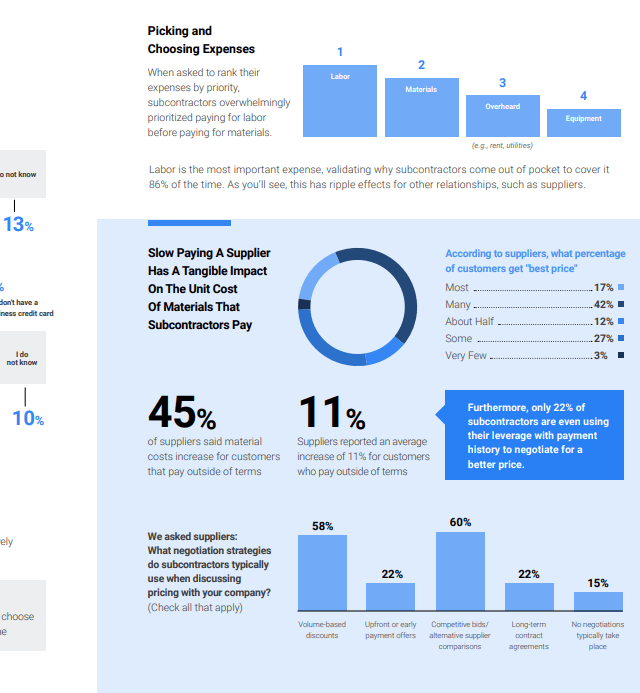

Furthermore, only 22% of subcontractors are even using their leverage with payment history to negotiate for a better price.

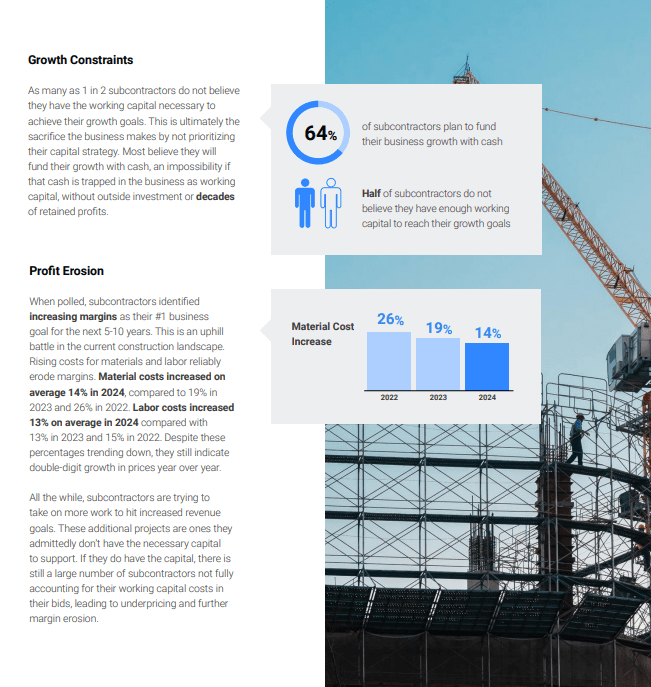

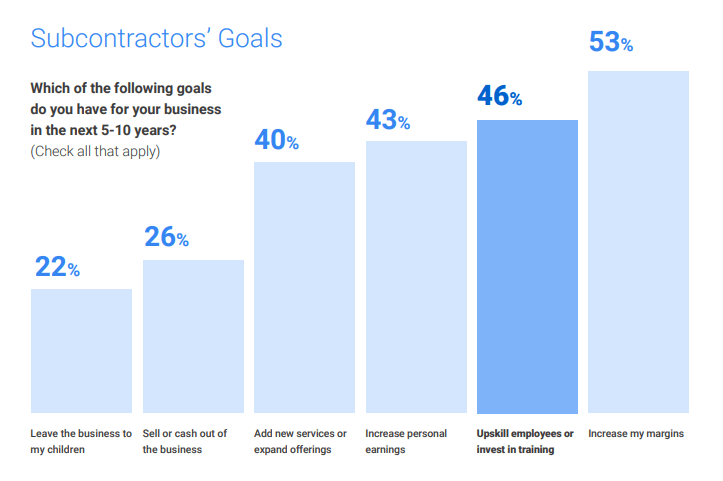

When polled, subcontractors identified increasing margins as their #1 business goal for the next 5-10 years. This is an uphill battle in the current construction landscape. Rising costs for materials and labor reliably erode margins. Material costs increased on average 14% in 2024, compared to 19% in 2023 and 26% in 2022. Labor costs increased 13% on average in 2024 compared with 13% in 2023 and 15% in 2022. Despite these percentages trending down, they still indicate double-digit growth in prices year over year.

All the while, subcontractors are trying to take on more work to hit increased revenue goals. These additional projects are ones they admittedly don’t have the necessary capital to support. If they do have the capital, there is still a large number of subcontractors not fully accounting for their working capital costs in their bids, leading to underpricing and further margin erosion.

Despite GCs contributing to slow pay, they still hold the expectation that subcontractors should have robust financial resources to cover multiple project costs. When subs mismanage their capital, it ultimately hurts their performance in the eyes of the GCs.

Subcontractors may believe they are getting the best unit prices by shopping suppliers against one another. But in reality, suppliers are factoring in the costs of not being paid on time, so the “best price” one subcontractor sees might be more than another who pays on time. In other words, a subcontractor who pays within their net 30 terms gets a better price on materials than one who waits to pay until day 60, making the first sub’s bid more competitive than the one who takes longer to pay.

When asked to describe what unhealthy growth looks like, subcontractors overwhelmingly pointed to cash flow issues as a key indicator. However, the challenges of uncontrolled growth extend far beyond cash flow, affecting nearly every aspect of operations and long-term sustainability

Subcontractors frequently cited terms like “cash flow problems,” “cash deficits,” and “cash is tight” when describing unhealthy growth. These issues manifest as businesses running out of working capital, struggling to pay invoices on time, or being unable to finance day-to-day operations.

Unhealthy growth often forces businesses to over rely on credit. Subcontractors mentioned “maxing out bank lines of credit,” being “over-leveraged,” or having “too much reliance on credit.” This financial instability makes it difficult for businesses to use debt in a more effective way that would ultimately enable sustainable growth.

Subcontractors described being “overextended” or “stretched too thin,” at which point inefficiencies and missed deadlines abound. Terms like “chaos,” “disorganized,” and “stressful” highlight the operational struggles that accompany rapid growth.

Growth places significant pressure on employees and management. Subcontractors reported challenges such as “rushed hiring,” unsustainable workloads, high employee turnover, and burnout. This strain can diminish morale and productivity.

Mentions of “poor quality,” “defects,” and a “loss of workmanship” underline how rapid growth can compromise project outcomes. Businesses noted that customer satisfaction declines as delays, defects, and rushed work become more common— often resulting in rework or reputational harm.

Unhealthy growth often results in shrinking profit margins, as businesses take on more work than they can efficiently finance or manage, leading to rising costs and reduced profitability

Uncontrolled growth can lead to missed opportunities due to overcommitment or resource shortages. Subcontractors reported losing projects because they didn’t have enough resources to meet demand. In extreme cases, businesses cited outcomes like bankruptcy or described it as the “beginning of the end.” This highlights not only the risk of running out of money, but also the inability to seize opportunities due to financial constraints—a critical insight.

Cash is king–and it should be something reserved for reinvestment and growth. However, it cannot do all the heavy lifting on its own.

While problems like slow pay may be universal, surrenduring to them is not. Thousands of subcontractors have found strategic ways to work around the burdens of the industry without compromising their financial health. These subcontractors account for their working capital costs as part of a smart capital strategy. Last year’s report showed that this subset of subcontractors was already performing better than their peers, and this year’s report shows that their upward trajectory was no one-off. This year’s findings show the divide in profitability continues to grow. These businesses and their owners consistently do better on all counts, and their habits can (and should) be replicated.

By building a robust portfolio of working capital options, regularly requesting limit increases, seeking new credit well before they need it, and being open to newer forms of industry financing, subcontractors are better positioned to withstand industry norms like slow pay. They can more readily accept larger projects knowing they have the financial arsenal to endure project demands.

Here are three ways top-performing subcontractors are creating a capital strategy that empowers them to succeed.

Construction-specific financial solutions play a critical role in creating a healthy capital stack. These financial solutions, including Pay App Advance and material financing, offer flexible terms aligned to industry timelines, giving subcontractors more time to collect payment before paying their own invoices.

Using financial data that is already at their disposal, financially savvy subcontractors are able to determine what it costs to fund their projects. Knowing your true cost of capital is the first step to accounting for it.

Calculating and accounting for the cost of capital in bids sets subcontractors apart, making them more profitable. This is not a universal practice among subcontractors, but it should be.

As mentioned earlier, subcontractors rely on a variety of negotiation tactics to lower the cost of materials. These include volume-based discounts, upfront or early payment offers, alternative supplier comparisons, and long-term contract agreements. In this context, using construction-specific financing offers subcontractors new negotiation leverage, as they can sometimes secure 1-7% discounts on purchases when they pay up front with material financing.

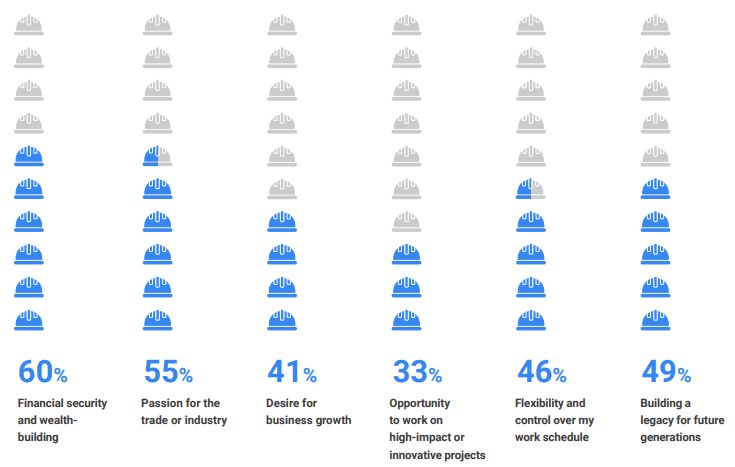

The motivations behind owning a subcontracting business are diverse and multifaceted, reflecting both personal and professional aspirations. The survey revealed a mix of drivers that inspire individuals to become and persevere as commercial subcontractors, as well as diversity in the types of goals these owners hope to accomplish in the future.

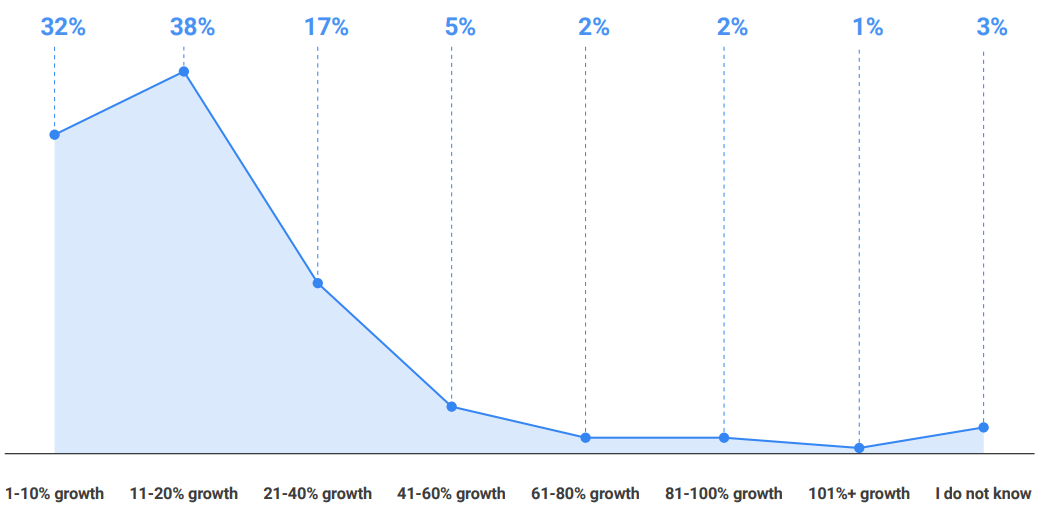

The outlook around business growth remains optimistic year over year.

The 2025 National Subcontractor Market Report paints a picture we already know: there is a long-standing structural flaw in the way subcontractors are paid in commercial construction.

This year, the report sheds light on the disconnect between the GC and subcontractor about how they view the problem. When polled, GCs put the average DSO at 30, while subcontractors report 56 days on average. More troubling is that subcontractors don’t know if payment will come on day 30 or day 56. The only thing predictable is that payment for subcontractors’ work is unpredictable. This forces them to take a new approach to working capital. Their best solution: a proactively-planned capital strategy.

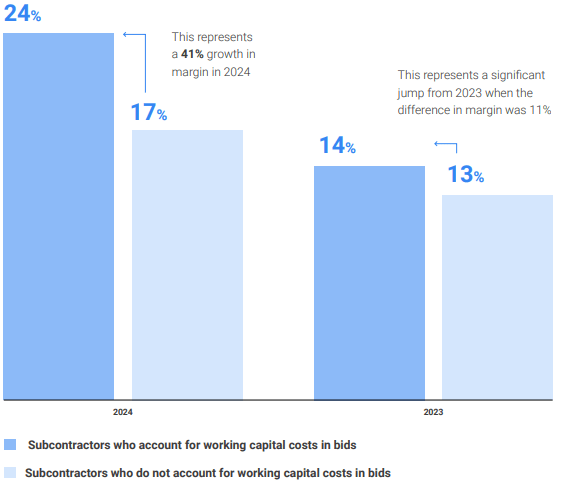

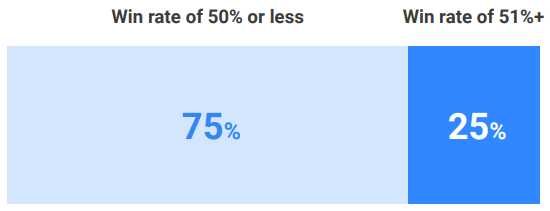

In the report you’ll see the benefits of one particular proactive practice: leveraging multiple sources of working capital AND accounting for them as real project costs. Subs who factor working capital costs in their bids see 41% greater profitability. It’s a number we can’t celebrate enough. That can be the difference between surviving and thriving, between stagnation and growth. And the best part? They’re winning more bids too.

As the Champion of the Sub, Billd has made it our mission to shine a light on the severity of the problem and offer proof that there are solutions. Subcontractors have been forced to capitalize their businesses through options that simply do not give them enough capacity to work around 56-day payment— including 30-day supplier terms and using retained profits to overcome the working capital gap. They’re actively combatting the unpredictable cycle rather than applying their capital and efforts towards growth.

Thankfully, we talk to subs daily who are taking a strategic approach to working capital in order to combat the effects of poor cash flow, unlocking profitability and sustainable growth. Our hope is that this report can help subs of all sizes make a change—whether that’s implementing a whole new capital strategy from scrat

Christopher Doyle is an entrepreneur and business leader with extensive construction and finance industry experience. He is the co-founder and CEO of Billd, a disruptive payment solution for the construction industry that helps subcontractors grow their businesses with less hassle and risk. Recognizing the cash flow hurdles that contractors face, Doyle launched Billd to make traditional Wall Street working capital accessible to business owners in the construction industry.

Billd stands alone as a partner that truly champions the subcontractor. Their financial and payment products empower subcontractors to bypass project hurdles by providing access to upfront funds to cover their most pressing costs, including materials and labor. Unlike traditional financing outlets, Billd provides flexible lines of credit to accommodate the unpredictability of cash flow in construction, and extends their customers up to 120-day terms to align with industry payment standards. Billd knows traditional credit metrics are poor predictors for risk and has built a variety of industry-specific, proprietary analytic and financing tools to allow subcontractors to stabilize cash flow and more effectively grow their businesses.